We are committed to replying to you in a timely manner, please allow at least one business day for a response. Do not share any personal information such as account numbers, social security numbers, or other sensitive information using this web form.

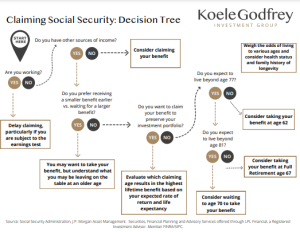

Deciding when to retire and begin collecting Social Security is an important life decision. For some, savings losses may dictate that you delay your retirement plans and continue working, which means postponing when you begin collecting Social Security.

Current law allows workers to begin collecting Social Security between 62 and 70 years of age. The longer you delay retirement, the higher your monthly Social Security payout will be. That payout is based on your earnings history and the age at which you begin collecting payments compared to what the government deems the normal retirement age (NRA), which depends on your birth year.1

Year Born

Normal Retirement Age

1937 or earlier

65

1938

65 and 2 months

1939

65 and 4 months

1940

65 and 6 months

1941

65 and 8 months

1942

65 and 10 months

1943-1954

66

1955

66 and 2 months

1956

66 and 4 months

1957

66 and 6 months

1958

66 and 8 months

1959

66 and 10 months

1960 or later

67

If you choose to begin collecting Social Security before your NRA, you may receive a reduction in monthly payments by up to 30%. Additionally, if you begin collecting early and you continue to earn income that exceeds the annual earnings limit, you will incur a penalty.

On the other hand, if you delay collecting Social Security until after your NRA, you will receive higher monthly payments. For each month past your NRA that you delay retirement, your monthly Social Security benefit will increase 0.29% if you were born between 1925 and 1942, and 0.67% if you were born after 1942.

So should you retire early, late, or exactly at your NRA? That depends on your financial situation and anticipated life expectancy. If you have a strong pension or hefty savings, you may wish to delay retiring.

If you have a family history of longevity, you will receive higher payments if you delay receiving benefits. For instance, if you think that you’re unlikely to live beyond 80, you may want to begin collecting Social Security at age 62. But if you expect to live longer than 82, you might consider delaying Social Security benefits.

Whenever you decide to begin collecting Social Security, remember that it represents roughly one-third of retirees’ income,2 according to the Social Security Administration. So you should consider other savings strategies to help support you when you decide to retire.

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal.

This material was prepared by LPL Financial, LLC.

There’s a simple word that has profound implications for savings and investing: compounding. Like a snowball that grows as it rolls down a hill, compounding provides the potential for your money to grow, reinvesting your investment earnings.

It is a basic model for growth potential, and the more you invest, the greater the opportunities to create long-term value. Let’s take a look at some hypothetical examples1 to illustrate:

If you invest $1,000 at age 20 and do not add anything to the principal, relying instead on 7.2% annual earning growth, you would end up with $32,000 at age 70.

If you wait until you’re 30, though, investing that same $1,000 that earns 7.2% annually, you would end up with $16,000 at age 70 — a decrease of 50%.

Finally, if you invest the $1,000 at age 20, earning 7.2% annually while contributing $83 a month until retirement, you would have $465,000. (This is a hypothetical example and is not representative of any specific situation. Your results will vary. The hypothetical rates of return used do not reflect the deduction of fees and charges inherent to investing.)

Calculating the Impact of Compounding

To estimate how long it will take for compounding to double an investment, use the rule of 72:

Divide 72 by the annual rate of return. The answer is the approximate number of years it would take to double your investment’s value, assuming a fixed rate of return.

As an example, if you earn 9% annually, it will take 72/9 = 8 years to double the value of your investment. Please note, the rule of 72 is a mathematical concept and does not guarantee investment results nor functions as a predictor of how an investment will perform. It is an approximation for the impact of a targeted rate of return. Investments are subject to fluctuating returns and there is no assurance that any investment will double in value.

The Long-Term Effect

Adopt a strategy to maintain your portfolio for the long-term, it can help you emotionally ride out the short-term effects of sharp market swings.

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal.

Past performance is no guarantee of future results.

This material was prepared by LPL Financial, LLC

Individual retirement accounts (IRAs) are one of the most common assets people rely on to save and invest for retirement. In fact, more than a third of households in America own an IRA. If you’re thinking of opening an IRA for the first time, it’s a good idea to review the rules. Even if you have had an IRA for years, note that laws change.

The Different Types

There are two main types of IRA accounts to choose from: traditional and Roth. The timing of the tax advantages is the main difference between the two. For a traditional IRA, contributions are tax deductible and tax is paid upon withdrawal. Roth IRA contributions are taxed in the year they are made, and qualified withdrawals are tax-free. Both types are almost equally popular:

36% of American households have Roth IRAs

35% of American households have traditional IRAs

26% of American households contribute to both

There are also employer-sponsored IRAs. These may fall into either of the two categories.

Contribution Limits

The IRS set a 2020 annual limit of $6,000 for people under 50 years old. People who are 50 years and older can make a total contribution of $7,000. What some breadwinners do to maximize contributions is to file joint tax returns and open a second account for their spouses. They then make additional contributions to this account. The IRS states that the combined contribution cannot exceed the lesser of the couple’s taxable income or the contributor’s individual limit times two.

Eligibility

The IRS considers net income from self-employment, gross wages, and gross salaries as qualifying income. Too much income, however, and IRA contributions can get reduced or prohibited altogether:

Qualifying Widower or Married Filing Jointly: The regular contribution rules apply up to $196,000. From $196,000 to $206,000, the IRS reduces the contribution limit. No contributions are allowed after $206,000.

Single, Married, Filing Separately (did not live together), or Head-of-household: Filers who earn less than $124,000 follow the usual contribution rules. More than this up to $139,000, the IRS reduces the contribution limit and after $139,000, contributing is not allowed.

Married Filing Separately (lived together): The IRS reduces the contribution amount for less than $10,000 and prohibits contributions for $10,000 in income or more.

Tax Deductions

How much income you make determines how much of your total contribution you can deduct from your taxable income and whether or not you contribute to an employer sponsored retirement plan:

Qualifying Widower or Married Filing Jointly: Filers who make $104,000 or less can take tax deductions up to the full contribution limit. More than this, up to less than $124,000, people can get a partial deduction. Beyond this, there is no deduction.

Single or Head-of-household: For total incomes of $65,000 or less, the individual can take the full deduction. More than this, up to less than $75,000, there is only a partial deduction. Beyond $75,000, there is no deduction.

Married Filing Separately: There is a partial deduction for income up to $10,000. After $10,000, there is no deduction.

Distributions

Like any retirement account, you do not need to wait until retirement to claim your distributions. Here’s what you need to know:

There is no penalty for traditional IRA withdrawals after reaching age 59 and a half.

Traditional IRA distributions get taxed at the rate that is current at the time of withdrawal.

Roth IRA withdrawals are not taxed because taxes were already paid upfront.

Roth IRAs do not have mandatory withdrawal rules, but traditional IRAs require distributions by April 1st of the year you turn 72 or there are considerable tax penalties.

Traditional IRAs are funded with tax-deductible contributions in which any earnings are tax deferred until withdrawn, usually after retirement age. Unless certain criteria are met, IRS penalties and income taxes may apply on any withdrawals taken from Traditional IRAs prior to age 59 ½. RMDs (required minimum distributions) must generally be taken by the account holder within the year after turning 72.

The Roth IRA offers tax deferral on any earnings in the account. Withdrawals from the account may be tax-free, as long as they are considered qualified. Limitations and restrictions may apply. Withdrawals prior to age 59 ½ or prior to the account being opened for 5 years, whichever is later, may result in a 10% IRS penalty tax. Future tax laws can change at any time and may impact the benefits of Roth IRAs. Their tax treatment may change.

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal.

This information is not intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor.

This material was prepared by LPL Financial, LLC.

When it comes to financial stability, people tend to focus on paying off debt and saving for retirement. In reality, many other financial goals beckon to individuals during their lifetime. Because of this, it’s important to look beyond retirement when setting targets, no matter how old you are.

Identify Future Objectives

While it is never too early to start planning for retirement, waiting until you reach 65 years or older to truly live is a mistake many people come to regret. A number of exciting possibilities are waiting for you throughout your life:

Building an emergency fund

Creating and growing passive income

Starting a business

Owning a home

Becoming debt-free

Raising a family

Consider Income

Some people start their careers making six figures or more, but this is rare. By about 25 years old, making $35,000 or so is a reasonable expectation. If your salary increases following the historical rate and you have no major employment gaps, you could earn almost $2 million by the time you’re ready for retirement.

Without a doubt, $2 million is a lot of money. If you take a second look at the list of potential financial goals, however, it begins to lose its comparative value. For instance, the current cost of a starter home is anywhere from $150,000 to $250,000. Similarly, student loans are one of the biggest obstacles to a debt-free life. The average student loan debt is $29,800.

Create a Plan

If you’re starting to feel discouraged, the good news is that money isn’t a static asset. It has the potential to grow and do some of the work for you by creating passive income. In fact, people who begin to invest in their future early can better position themselves in the pursuit of their retirement goals. You can employ several different strategies to help your money go further:

Designate a portion of raises: Instead of increasing living expenses to match any pay increases, try to retain the original budget as much as possible and invest the extra. Keep the same starter home you bought. Drive your present car for as long as possible.

Start small: Not everyone is making $35,000 per year at age 25. Some people make significantly less throughout their earning years. The answer to this economic problem is to start small. Save $100 per month if you can and $10 per month if you can’t. It all adds up, especially when properly invested. In 10 years, $100 per month at a 6% annual return could potentially grow into $15,996. (This is a hypothetical example and is not representative of any specific situation. Your results will vary. The hypothetical rates of return used do not reflect the deduction of fees and charges inherent to investing.)

Buy wisely: When you purchase a vehicle or buy a home, consider the maintenance cost and tax breaks. For instance, is it better to invest in solar panels than a new sunroom for your home? Likewise, consider the potential tax or economic benefits of a small electric vehicle or hybrid over a new mid-size SUV.

Make use of programs and incentives: There are many financial products and accounts available that could help you invest your money in a tax-efficient manner. These include HSA accounts, 401(k)s, Individual Retirement Accounts (IRAs), and 529 college savings plans. Taxes can have a big impact on passive income. It is important to manage their impact over a lifetime.

Reduce Debt

The best time to start minimizing debt is before you take any on. This does not mean you should never buy anything on credit. It does imply wisdom in how you use debt. Also, be wise about payment terms, interest rates, and the types of debt.

Whenever possible, pay down that debt as quickly as you can. However, never become so focused on paying off debt that you neglect your savings. Take yet another look at the list of potential financial goals. There is more to life then repaying big corporations.

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal.

This material was prepared by LPL Financial, LLC

There’s a good reason so many athletes, entertainers, and business people who made seven figures and higher suddenly find themselves filing for bankruptcy. Money mismanagement can eat through even the biggest bankrolls. Here are some specific threats to financial stability that people can avoid to help effectively manage their wealth.

No Budget

In 2019, CNBC reported that even though 93% of Americans believe everyone should have a budget, only one in three actually do. Budgeting does not have to mean skipping coffee and driving a jalopy for the rest of your life. It does mean paying close attention to how much money comes in and where it all goes. Use your financial goals to guide you in steering your money in the right direction.

Too Much Debt

If you have a lot of debt to pay off, a budget is all the more important. It helps reduce the likelihood of relying on more credit to fill the gaps. A budget also helps you to collect all those extra dollars and cents that you could put toward paying more than the bare minimum on debt. When paying off debt, start with the higher-interest accounts first and work your way through to save money.

No Protection

Insurance can be expensive, but going without insurance can be even more so. Renters, homeowners, auto, health, disability, and life insurance policies are the main ones you should consider. If you have a business — especially if it is your main or only source of income — getting business insurance can protect your livelihood in the event of a mishap with a client or customer.

No Retirement Planning

Forbes estimates that roughly 25% of Americans have nothing saved for retirement. This may be forcing some people to continue to hold stressful, low-paying jobs well into their retirement years. It is never too early to start planning for retirement, no matter how small your contributions are. Remember to take advantage of matched contributions from employers whenever possible.

Too Much Risk

There is no investment that is 100% without risk. If there were, the returns on that investment would be negligible. Even so, taking on too much risk at the wrong time can lead to big financial problems. Taking on high levels of risk is appropriate for young people who have more time to recover and is not advised for people nearing retirement.

Shady Investments

Even worse is when risky investments turn out to be fraudulent or shady. In fact, the more risk-free an investment sounds, the more you should do some digging. This holds true whether the business or individual you plan to invest in is a stranger or your brother. People who miscalculate or fail to do enough research can cause you just as much financial damage as fraudsters.

Poor Tax Management

No matter how much or how little money you make, tax management is a great way to help keep money in your pockets. This is especially important after a large windfall, such as an inheritance. For instance, if you inherit an Individual Retirement Account (IRA) and choose to cash out, you may lose a portion of this in taxes. Divorce is another time of life when tax management is key.

Mismanaged Assets

Stocks are often traded frequently, making them active investments, but you still need to ensure your portfolio stays balanced. Similarly, if you have a home, keeping up with repairs and improvements maintains and grows its value. Unmanaged assets also pose a problem, such as when people allow large sums of money to sit in accounts with low to no interest rates and high fees.

For some people, money management is a talent and financial literacy is almost an inborn skill. Many other people, however, could use a little help making financial decisions. Contact us to speak with professionals who can help to steer your finances in the right direction.

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal.

This material was prepared by LPL Financial, LLC

Only about 23% of American workers say they are "very confident" they will have enough money to live comfortably throughout retirement.1 To help reduce such uncertainty in your life, consider these five common investment pitfalls – and how you might avoid them.

Mistake #1: Waiting to Maximize Your Contributions

The sooner you start contributing the maximum amount allowed by your employer-sponsored retirement plan, the better your chances for building a significant savings cushion. By starting early, you allow more time for your contributions – and potential earnings – to compound or build upon themselves, on a tax-deferred basis.

Mistake #2: Ignoring Specific Financial Goals

It is difficult to create an effective investment plan without first targeting a specific dollar amount and recognizing how much time you have to pursue that goal. To enjoy the same quality of life in retirement that you have become accustomed to during your prime earning years, you may need the equivalent of 80% or more of your final working year's salary for each year of retirement.

Mistake #3: Fearing Stock Volatility

It is true that stock investments face a greater risk of short-term price swings than fixed-income investments. However, stocks have historically produced stronger earnings over the long term.2 In general, the longer your investment time horizon, the more you might consider adding stock funds to your portfolio.

Mistake #4: Timing the Market

Some investors try to base investment decisions on daily price swings. But unless you have a crystal ball, "timing the market" could be very risky. A better idea might be to buy and hold investments for several years.

Mistake #5: Failing to Diversify

Investing in just one fund or asset class could subject your investment portfolio to unnecessary risk. Spreading your money over a well-chosen mix of investments may help reduce the potential for loss during periods of market volatility. Diversification may offset losses in any one investment or asset category by taking advantage of possible gains elsewhere.3

Now that you are aware of these five common investment errors, consider yourself lucky– you are ready to potentially benefit from other people's experiences – without making the same mistakes.

1Source: Employee Benefit Research Institute, "The 2019 Retirement Confidence Survey," 2019.

2Source: SS&C Technologies, Inc. Stocks are represented by total returns from Standard & Poor's Composite Index of 500 Stocks, an unmanaged index generally considered representative of the U.S. stock market. Fixed-income investments are represented by annual total returns of long-term (10+ years) Treasury bonds. Indexes do not take into account the fees and expenses associated with investing, and individuals cannot invest in any index. Past performance is no guarantee of future results. With any investment, it is possible to lose money.

3Diversification does not ensure a profit or protect against a loss in any market.

Because of the possibility of human or mechanical error by DST Systems, Inc. or its sources, neither DST Systems, Inc. nor its sources guarantees the accuracy, adequacy, completeness or availability of any information and is not responsible for any errors or omissions or for the results obtained from the use of such information. In no event shall DST Systems, Inc. be liable for any indirect, special or consequential damages in connection with subscriber's or others' use of the content.

The LPL Financial registered representatives associated with this website may discuss and/or transact business only with residents of the states in which they are properly registered or licensed. No offers may be made or accepted from any resident of any other state.

Check the background of investment professionals associated with this site on FINRA’s BrokerCheck

Check the background of investment professionals associated with this site on FINRA’s BrokerCheck